House price predictions and rental trends for UK & London 2018

Kate Faulkner looks at the house price predictions for 2018 and how the potential market conditions might affect landlords. To read about our specialist landlord insurance, click here.

- House price predictions in 2018

- What is house price index

- UK house price growth over the past year

- UK house price growth forecast

- London house price forecast

- Have higher Stamp Duty rates and other tax changes slowed down the market?

- How could Brexit affect house prices

- The outlook for landlords in 2018?

- Buy to let in 2018

- Looking to 2018

House price predictions

Around this time each each year, economists and property professionals publish their property market predictions for the upcoming 12 months, giving investors their expert opinion on what the new year will bring.

Unfortunately, house price forecasts are notoriously difficult to get right, partly because of the extent to which the market can be affected by confidence. Domestic economic uncertainty and major world events can impact the property market within a matter of days, so it's no surprise that the ongoing Brexit negotiations and an unstable political situation are making it particularly hard to predict what lies ahead for 2018.

What is the house price index?

When it comes to reviewing house price forecasts, one thing to be aware of is that there are lots of house price indices that measure prices at different stages of the buying and selling process.

For example, some measure the price at which properties are marketed while others focus on properties that are mortgaged, which naturally leads to discrepancies between the various forecasts.

However, we do have nearly 20 years of data from the Land Registry, which has logged the actual sale price for individual properties through good times and bad. This data helps forecasters better understand and predict what is going to impact property prices rising or falling.

UK house price growth over the past year

This official Land Registry data breaks down by country and government office region. It shows that, while there isn't a huge discrepancy between the nations, the overall growth figure for England has been significantly better in the past due to London, but is currently being reduced by relatively poor performance after huge growth since the credit crunch.

| Country | Average price | Annual change |

| England | £244,000 | +5.3% |

| Wales | £150,000 | +3.4% |

| Scotland | £146,000 | +3.9% |

| N.Ireland | £129,000 | +4.4% (Yr to Q2 2017) |

| English Region | ||

| East Midlands | £183,762 | +6.4% |

| East of England | £288,440 | +6.4% |

| London | £484,362 | +2.6% |

| North East | £130,731 | +3.7% |

| North West | £159,865 | +6.5% |

| South East | £324,983 | +4.8% |

| South West | £251,984 | +6.4% |

| West Midlands | £188,447 | +5.3% |

| Yorkshire & Humber | £158,689 | +4.8% |

This generally steady growth across the UK reveals that 2017 has been strong and stable for the property market. Following years of post-credit crunch flux, when we saw a house price crash followed by big rises, it seems that people are now taking a longer-term view of an era of more subdued capital growth. This more relaxed attitude may also be a reflection of the fact that more than half of homeowners in the UK are mortgage free, so their decisions about buying and selling won't be as influenced by economic ups and downs.

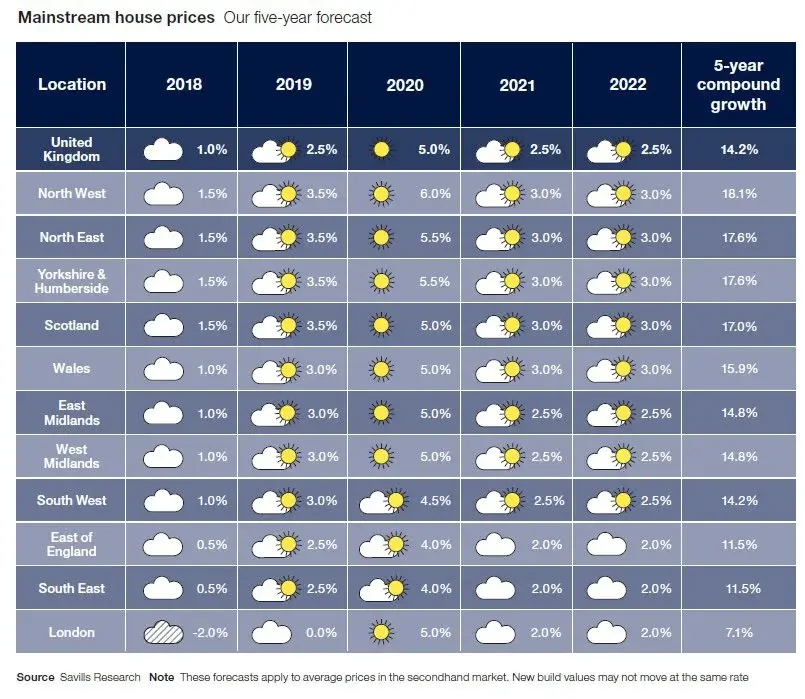

UK house price growth forecast

In figures published in November, Savills expects house price growth to slow in 2018, “as uncertainty weighs down the market. With the UK's future relationship with the EU up in the air, we've seen the UK's credit rating downgraded, the pound weakened, and the economy subdued. Inflation has cut into people's earnings, with the ONS reporting that incomes fell by 0.4% last year in real terms. Against this economic backdrop, there are no strong drivers for house price growth over inflation in 2018.”

Their forecasters are predicting growth of just 1% for the UK as a whole next year. The national breakdown is a 3/4 of a percent rise for England – brought down again by London, which they predict to fall by 2%, 1% for Wales, and 1.5% for Scotland. They see the strongest growth in England likely to be in the north, at 1.5%.

Looking further ahead, Savills believe there is capacity for growth but that it will be tempered by interest rate rises. With this in mind, they expect UK house price growth to total just 14% over the next five years – that's half the growth we've seen over the last five.

Knight Frank has been more optimistic, although its predictions were made in May of this year, before both the snap general election result and lack of any progress on Brexit had landed on our economic plate. Their forecasts for 2018 were that the average UK house price would rise by 2.5%, buoyed up by strong performances in the East Midlands, West Midlands and Yorks & Humber, all predicted to increase by 3%.

Countrywide, which published its forecasts in the summer, falls between the predictions made by Savills and Knight Frank. Their experts suggest 2% growth for Britain, with the North East at the bottom of the table at 1% and, interestingly, London and the South East at the top, at 2.5%.

Meanwhile, back in April, the Centre for Economics and Business Research (CEBR) predicted a 4.1% increase in 2018.

London house price forecast

In their summer economic report, Strutt & Parker stated they expect prices in the capital to remain flat through 2018. They believe that most of the fallout from Brexit, and the stamp duty increases, has now been experienced by the prime market and that the outlook for the UK 'remains reasonable'.

Meanwhile, the forecast from Savills is that London prices will fall by 2%, while Knight Frank believe they will rise by 2%. Countrywide is the most optimistic, predicting that prices will rise by 2.5% in Greater London, with the Prime Central London market increasing by 4%. This is chiefly because they believe that after two consecutive years of falls in 2015 and 2016, a recovery is overdue.

The reason for Savills' negative prediction seems to be a firm belief that mortgage regulation, affordability, and increased stamp duty costs have simply limited the number of people who are able to buy in London. According to their research, only 28 of its 600 wards or neighbourhoods have an average house price of less than £300,000 and, with mortgage regulation having the intended effect of preventing borrowers from taking on excessive debt, the market has been forced to slow. They predict that capital growth in London will feel the drag of interest rates creeping up and the continuing stress testing of buyers' affordability for several years to come.

Have higher Stamp Duty rates and other tax changes slowed down the market?

It seems clear that government intervention in the market has had, and is continuing to have, a dampening effect in some areas. The prime market in particular is suffering because of higher stamp duty levels and, according to a December 2016 survey by the Council of Mortgage Lenders, more than a quarter of landlords plan to reduce their portfolio or leave the market in the next one to five years, with 15% citing tax changes as the reason.

The more expensive London market is suffering from higher rates, with the average stamp duty bill in London for 2016/17 standing at £25,703 – that's more than three times the average bill for England. One of the reasons Savills gives for the growth in the North of England is that the initial cost of acquisition is significantly cheaper. According to their figures, the average SDLT paid in the North West in 2016 was 2%, compared to 5% in London - that's £3,000 versus £25,700 in average real terms. Together with more stringent lending criteria having an effect on affordability in general, stamp duty certainly seems to be having an effect on what and where people are buying.

Much is often made of the stamp duty tax on second homes, but two important things need to be remembered: firstly, it's tax deductible when you sell, and secondly, given that buy to let should be a 15-20 year investment, the total capital growth over that time should be sufficient to absorb the increased initial cost of purchase.

How could Brexit affect house prices?

The first thing to say is that the market in 2017 has been quite resilient in the face of predicted turmoil – in particular, the threat that legions of foreign investors would exit the UK market has largely failed to materialise. After the huge falls post-credit crunch, which were followed by huge rises as the market recovered in London, the South East, and East Anglia, we're now seeing a more stable market as demand and supply have started to match once again.

However, if the negotiations result in a less than favourable deal, or we experience an unstable transition period, there could be a knock-on effect on the housing market. Specifically, if London's status as a leading global financial hub is negatively affected by the end deal, the central and prime housing markets could suffer, certainly in the short term.

Nevertheless, the fundamental continuing shortage of housing supply and unwavering demand suggests that that market is unlikely to stray from its current 'strong and stable' path.

The outlook for landlords in 2018?

Figures from Savills show that there has already been a fall in the number of mortgaged investment property purchases made by investors and they predict there will be a drop of 27% over the next five years – down by 10,000 in real terms in 2018. This, they say, is due to the 'triple hit' of the extra 3% stamp duty, the restriction of tax relief on mortgage interest payments, and increased mortgage regulation. Given that we are only at the start of the staggered introduction of the reduced tax relief schedule and mortgage regulation for portfolio landlords, Savills predict that those who stay in the market will increasingly look for cheaper, higher-yielding properties in order to make the figures stack up, and that will mean landlords moving away from London and the South of England.

While the extra financial burden brought on by legislation is unlikely to let up in 2018, the ongoing pressure on affordability for prospective and existing homeowners means that well-capitalised and savvy landlords should be able to take advantage of some good deals in cheaper parts of the country, in particular from vendors who are under some time pressure to sell.

There are also likely to be some 'ready made' rental deals on the market, as a fifth of landlords have said they intend to sell in the next few years. The benefit of this kind of purchase is that if a landlord is keen to offload their investment, and especially if they've held it for a number of years and have little or no mortgage borrowing, buyers could strike a good deal for a quick purchase. Plus the property will be in ready-to-rent condition and could come with a sitting tenant, meaning instant income.

For those with four or more properties planning to expand their portfolios in 2018, it's vital to be prepared for the new portfolio lending criteria and monitor the value, income, expenditure and level of borrowing associated with each investment property. It's undoubtedly going to take longer to secure mortgage offers and if landlords are highly leveraged, due to historical high loan-to-value deals that were available, they may find that although they may want to buy, it's simply not possible. So for some, it could be worth considering reinvesting rental profits into paying off mortgage loans in 2018, to get them down to below 75% across the whole portfolio.

But, all in all, given that there continues to be a shortage of good-quality rented accommodation in most areas and a growing demand, landlords that can still make their investments stack up should be encouraged that buy to let is still likely to deliver a positive long-term investment proposition.

Buy to let in 2018

The financial and mortgage regulation burden on landlords is likely to result in a slowdown in the supply of new rental properties coming to the market, while the steady rise in demand is predicted to continue. Nevertheless, landlords, whether they want to or not, could struggle to increase rents during 2018 because wages are now rising at a slower rate than inflation. Although rents can rally above this level for a short period of time, they have yet to do so for long and therefore it is likely they will stagnant for most of the UK throughout 2018.

What could be the effect of landlords exiting the market?

In the CML's landlord survey, which was carried out in December 2016, 21% of the 2,517 landlords surveyed said they planned to exit the market completely within 5 years, with a further 6% looking to reduce their holdings. Although that sounds like a significant number and may suggest a drop in the supply of properties for rent, at least in the short to medium term, it's important to look at the distribution of properties between landlords.

- 62% of landlords own only one property and make up around 28% of the market.

- 7% of landlords own five or more properties and account for 38% of PRS stock.

- Only 6% of landlords with five or more properties plan to leave the market, while a quarter of them plan to increase their rental holdings.

- Of those with four properties, 9% plan to sell up but 23% say they'll expand.

What these figures suggest is it is more likely landlords with one property only could exit the market, rather than those with portfolios, and the latter may even absorb the stock from existing landlords, suggesting that although an 'exodus' is expected during 2018, it may not be at the level some are predicting.

Looking to 2018

The overall outlook is that 2018 will continue in much the same vein as 2017: stable, with steady growth, although at a lower level than 2017. Property prices are predicted to increase by an average of around 2%, with less variation between the regions than we've seen over the past few years, while rents are likely to see growth around the same level as wages.

From a landlord perspective, it could be that some bargains become available in certain areas, with activity in the South to be more subdued and investment heading more towards areas such as Manchester. There is a risk of poorer performance if further economic shocks occur or uncertainty around Brexit worsens. As a result, landlords would be wise to review their property versus other financial returns, appreciate lending criteria is tightening, and a lack of wage growth will make higher rents somewhat more difficult to enforce.

Kate Faulkner

Last Updated: 27th Feb 2019

Find out more about this author